If you’re lying awake wondering whether your timeshare is quietly wrecking your credit score, take a breath. You’re not alone, and you’re not powerless. This is one of the most common worries I hear from timeshare owners, and it deserves a clear, honest answer.

Here’s the short version: yes, a timeshare can affect your credit. But the full story is more nuanced than that. Let’s walk through it together, step by step, so you understand exactly where you stand.

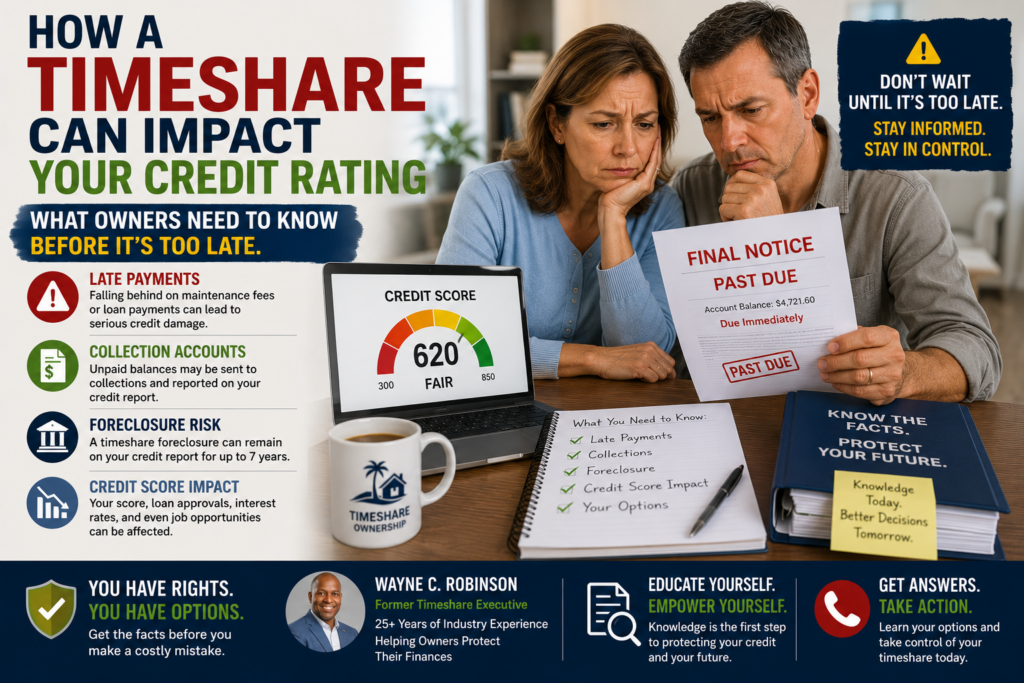

The Honest Answer: It Depends On Your Situation

A timeshare itself isn’t some magic credit-destroying object. It’s a contract, much like a car loan or a mortgage. How it affects your credit depends entirely on how you handle that contract.

If your timeshare is paid in full, you’re in a strong position. A fully paid timeshare carries no loan balance, so there’s nothing for a lender to report as missed or late. If you then cancel it the right way, through a legal exit process, it generally will not hurt your credit at all.

If you still owe money on your timeshare, the story changes. A balance on your account means there’s an active loan or financing agreement tied to your name. That balance behaves just like any other debt. Miss payments, and it can absolutely impact your credit.

This is the part many owners don’t realize until it’s too late. The maintenance fees, the special assessments, the loan payments. They’re all potential credit landmines if left unpaid.

What Happens If The Resort Files A Default

This is where things get serious. If you stop paying and the resort decides to take action, they can file a default against you. That default gets reported to the credit bureaus, just like a defaulted car loan or credit card would be.

A default doesn’t disappear quickly either. It can sit on your credit report for years, dragging down your score the entire time. That lower score can follow you into other parts of your life. It might affect your ability to refinance your home, get approved for a new credit card, or even qualify for certain insurance rates.

I’ve talked with hundreds of owners over the years who ignored their timeshare problem, hoping it would simply go away. It rarely does. Resorts and their collection departments are persistent, and once a default is on your record, the damage is done. You can’t simply ask it to be erased once it’s reported.

Why Ignoring The Problem Makes It Worse

Here’s something I want you to really sit with: if you ignore your timeshare situation, it may absolutely affect your credit. Silence doesn’t protect you. It just gives the problem more time to grow.

I understand the instinct to ignore it. Timeshare contracts are confusing, the maintenance fees keep climbing, and many owners feel embarrassed or overwhelmed by the whole situation. You bought something during a vacation, full of optimism, and now it feels like a burden you don’t know how to put down.

But every month that passes without a plan is a month closer to that default notice. Every unanswered call from the resort is a missed chance to get ahead of the problem. The timeshare industry counts on owners feeling stuck and doing nothing. Don’t give them that.

The Sooner You Act, The Better For You

I want to say this as plainly and as kindly as I can: the sooner you deal with this, the better it will be for you and for your credit rating.

If you’re still current on payments, you have options and time on your side. You can explore a legal cancellation process before any missed payment ever shows up on your report. That’s the best possible position to be in.

If you’ve already fallen behind, you still have options, but the clock matters more now. The longer a balance sits unpaid, the closer you move toward that default, and the more those marks pile up on your credit history. Acting now, even if it feels uncomfortable, puts you back in control.

What “Cancelling Legally” Actually Means

When I talk about cancelling your timeshare legally, I mean working through a proper, documented exit process. This is not about ignoring the contract, ghosting the resort, or hoping it fades into the background. It’s about formally and correctly ending your obligation, with paperwork that protects you.

A legal cancellation, done right, addresses your timeshare debt instead of leaving it hanging over you. That’s the difference between a clean exit and a credit disaster waiting to happen. When the process is handled properly, paid-in-full timeshares can be released without ever touching your credit.

This is exactly why I built my business around helping owners through this process the right way, instead of guessing their way through it or paying enormous fees to large exit companies promising the moon.

You Are Not Stuck, And You Are Not Alone

After 25 years in this industry, both on the resort side and now helping owners get out, I’ve seen every version of this story. Owners who panicked and did nothing, who got scammed by exit companies charging tens of thousands of dollars. Owners who finally took a small, smart step forward and felt the weight lift off their shoulders.

Your timeshare doesn’t have to define your financial future. A paid-off timeshare, cancelled the legal way, protects your credit completely. An unpaid balance, left ignored, puts your credit at real risk. The path you take from here makes all the difference.

If you’re reading this because you’re worried, that worry is actually a good sign. It means you’re paying attention, and that’s the first step toward fixing things. Don’t let fear or confusion keep you frozen. Your credit, your peace of mind, and your financial future are worth protecting.

Take that first step today, even if it’s just gathering your paperwork or asking an honest question. Every day you wait is a day the problem has room to grow. Every day you act is a day you take your power back.

Wayne C. Robinson is a retired U.S. Navy veteran, Certified Master Trainer, and 25-year timeshare industry veteran who now helps owners legally exit their timeshares for a fraction of the cost charged by large exit companies. Learn more at Everything About Timeshares.