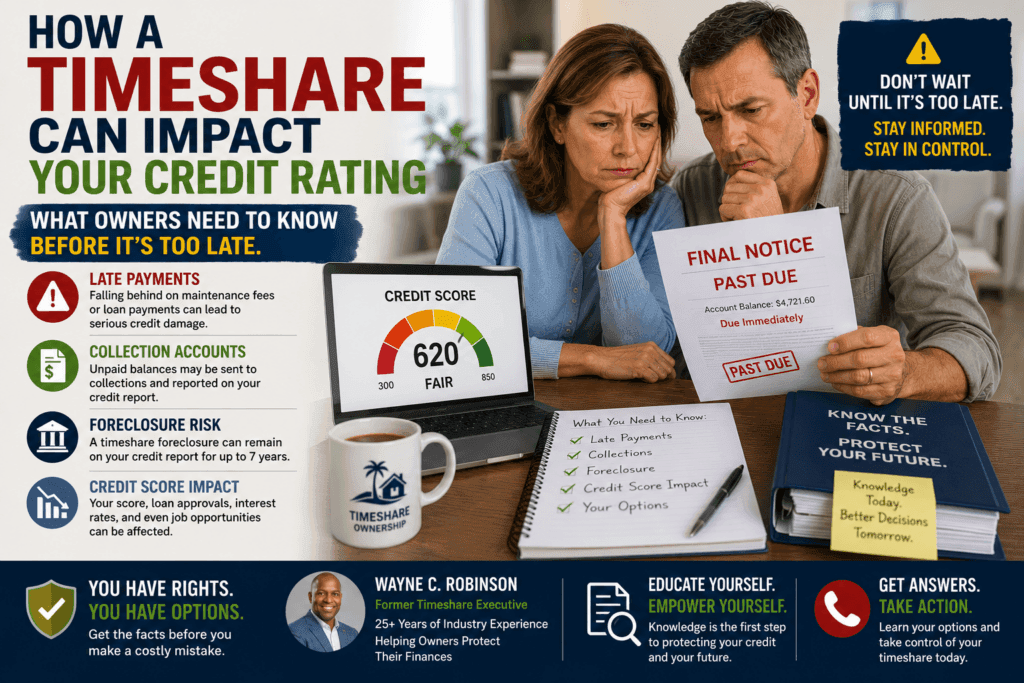

A lot of owners do not ask about the timeshare foreclosure credit impact until they are already behind on payments, maintenance fees, or both. By that point, the sales promises are long gone, the resale market is usually disappointing, and the notices from the developer or resort start to feel more serious. If you are in that position, the key is to understand what can happen before you decide whether to stop paying, negotiate, or pursue another exit path.

What timeshare foreclosure really means

In plain English, timeshare foreclosure usually means the resort developer, lender, or owners association is taking back the ownership because the account is in default. That default may come from unpaid loan payments, unpaid maintenance fees, special assessments, or a combination of those obligations.

This is where many owners get confused. A timeshare can involve two separate financial issues. One is the purchase loan, if you financed through the developer or another lender. The other is the ongoing obligation to pay annual maintenance fees, whether you still owe on the loan or not. You can be current on one and behind on the other, and each can create different credit consequences.

Unlike a traditional home mortgage foreclosure, a timeshare foreclosure is tied to a vacation ownership interest that often has very little resale value. But that does not mean the default is harmless. The account may still be sent to collections, reported to credit bureaus, or pursued under the contract terms you signed.

The real timeshare foreclosure credit impact

The timeshare foreclosure credit impact depends on how the account is structured, who is reporting it, and what stage of default you are in. There is no single answer that fits every owner.

If you financed the purchase and stop paying, the lender may report late payments first. Those delinquencies can hurt your score before foreclosure even happens. If the account continues in default, the lender may then report a serious derogatory event such as charge-off, repossession, or foreclosure, depending on its internal reporting practices and how the account is coded.

If the issue is unpaid maintenance fees, the resort or association may not report directly to the credit bureaus at first. Many do not. But they may turn the account over to a collection agency or law firm, and that is often when the credit damage starts to show up more clearly.

For some owners, the biggest hit comes from collections rather than the foreclosure label itself. For others, the lender reporting a defaulted loan causes the more immediate damage. Credit scoring is not perfectly transparent, so nobody should promise an exact point drop. What is fair to say is that serious delinquencies, collections, charge-offs, and foreclosure-related reporting can all lower your score and remain on your credit report for years.

Why some owners see credit damage and others do not

This is one of the most misunderstood parts of the issue. Owners often hear stories from other people who stopped paying and claim their credit was never affected. That can happen, but it should not be treated as a reliable outcome.

Some resorts pursue collections aggressively. Others focus mostly on recovering the interval or points and do less reporting. Some developers finance in-house and report like a major lender. Others rely on third parties. Some associations are more likely to sue for unpaid fees, while others are more likely to foreclose administratively and move on.

State law matters too. So does the wording of the contract. A deeded timeshare may be handled differently from a right-to-use product, and judicial versus nonjudicial processes can create different timelines and records. The bottom line is simple: do not assume your experience will match someone else’s.

What may show up on your credit report

Late payments and default reporting

If you have a financed timeshare loan, missed payments can appear the same way other installment delinquencies do. Thirty-day, sixty-day, and ninety-day late marks can build over time and drag down a credit score.

Collection accounts

When maintenance fees or loan balances are sent to collections, a collection account may appear on your report. Even if the original creditor never reported, the collector might.

Charge-offs, repossession, or foreclosure language

Different lenders use different reporting terms. Some timeshare accounts are reported more like unsecured or installment debt, while others may use terms related to repossession or foreclosure. Consumers tend to focus on the label, but the practical issue is the same: it is a serious negative item.

Public record or legal action in some cases

Not every foreclosure becomes something you will easily spot as a public record on your consumer credit file, but lawsuits, judgments, or related legal actions can create additional financial problems depending on the jurisdiction and the creditor’s strategy.

Can you still get a mortgage or car loan later?

Possibly, yes. But expect tougher terms if the derogatory marks are recent. A timeshare default does not make future borrowing impossible, but it can affect mortgage approval, interest rates, refinancing options, credit card approvals, and even insurance pricing in some situations.

Lenders usually care about the overall picture. If the timeshare foreclosure happened years ago, your other accounts are clean, and your income and debt levels look stable, the damage may be manageable. If the default is recent and part of a broader pattern of missed payments, it becomes a much bigger underwriting concern.

This is why timing matters. Owners sometimes stop paying without understanding that they plan to buy a home, refinance, or finance a vehicle within the next 12 to 24 months. That is when a short-term relief decision can create a much more expensive long-term problem.

What to do before you stop paying

Review what you actually own

Before making any move, confirm whether your ownership is deeded or right-to-use, whether there is an outstanding loan, and whether the default issue is tied to financing, maintenance fees, or both. Many owners are making decisions based on assumptions instead of the contract.

Ask the resort about surrender or deed-back options

Some developers and associations have formal surrender, deed-back, or voluntary relinquishment programs. Not everyone qualifies, and some programs require the loan to be paid off first, but it is always worth checking before choosing default.

Get clear on the balance and the reporting risk

Ask who owns the loan, whether the account is being reported, and what happens if payments stop. They may not give you every detail, but the answers can help you evaluate the risk more realistically.

Be careful with exit company promises

This is where owners often get hurt twice. A company may tell you to stop paying immediately, suggest the resort cannot affect your credit, or imply foreclosure is no big deal. That advice may be reckless, especially if the company has not reviewed your documents or explained the downside.

At Everything About Timeshares, this is one of the most common problems we see. Owners are sold certainty in situations that are full of variables.

If you are already in default

Do not ignore notices. That does not mean you need to panic or agree to the first demand, but silence usually makes the situation worse. Gather your contract, account statements, payment history, and any letters from the lender, HOA, or collection agency.

Then determine what stage the account is in. If it is only mildly delinquent, there may still be room to catch up, negotiate, or request a voluntary exit. If collections or foreclosure are already underway, your options may be narrower, but you still need accurate information before taking the next step.

It can also help to review your credit reports directly. That shows you what is already being reported rather than relying on guesswork. If inaccurate information appears, dispute procedures may be available, but they will not erase legitimate defaults.

Is foreclosure ever the least-worst option?

Sometimes, yes. That is the honest answer.

If the timeshare has no realistic resale value, the loan cannot be settled affordably, the maintenance fees keep rising, and there is no legitimate surrender option, some owners decide that accepting the credit damage is preferable to throwing more money at a failing obligation. That is not ideal, and it should not be romanticized, but it can be a rational decision in the right circumstances.

The mistake is treating foreclosure as automatically harmless or automatically catastrophic. For one person, it may be a manageable hit during retirement with no major borrowing plans ahead. For another, it may interfere with a home purchase, a refinance, or a debt recovery plan that depends on preserving credit.

The smart move is not to react emotionally to pressure from a resort or a third-party exit firm. It is to measure the likely financial fallout against the real alternatives in front of you.

If you are weighing a default, slow down long enough to get the facts. A timeshare problem is frustrating, but a rushed decision can follow you a lot longer than the vacation ownership itself.

Not sure where you stand? Start with a free review. If you’re trying to figure out whether you’re in default, what’s actually reportable, or whether a surrender or deed-back option might apply to your situation, don’t guess. I offer a free timeshare review where I’ll look at your contract and your situation and tell you honestly what your options are — no pressure, no upsell games. After 15 years inside the timeshare industry, I’ve seen how owners get hurt by bad advice from exit companies. My goal is simply to make sure you have the facts before you decide anything. [Request your free review here] https://gettimesharedebtrelief.com/free-timeshare-review/